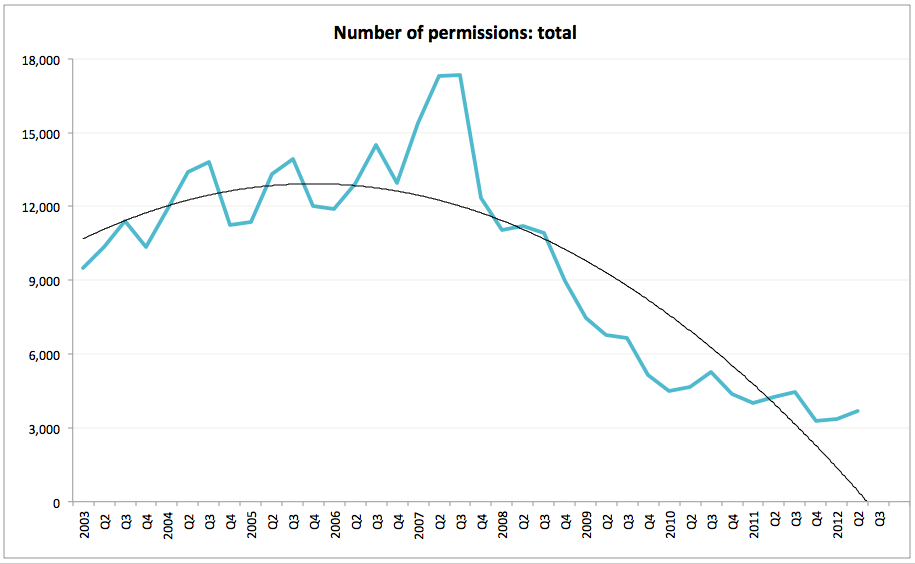

Ireland has one of the highest and healthiest birth rates in the advanced economies club, a fact that remains valid even today, amidst the economic downturn. In the past, this has prompted some economists and commentators to label this trend 'the demographic dividend'. I always pointed to the fact that if this indeed is a 'dividend', then retaining it within the Irish economy (society) is as important as generating it in the first place. Alas, over the recent years, our demographic dividend has been largely squandered away by the combination of a cyclical downturn (temporary loss of jobs) and more importantly by the structural recession (longer term loss of jobs). I highlighted the top line trends in our migration in the previous posts (here and here).

Here, let's take a quick look at the 'demographic dividend'.

With many caveats, let us define two groups of population: those in active working age group (20-64 years old) and those outside this group (0-19 years old and over 65 years old). The reason for these definitions is that younger people under 20 years of age are significantly engaged in education systems and although some of the students do work, they are not engaged in career-enhancing work and/or work part time. Similarly, some of the people in age category over 65 are still very much gainfully employed, but vast majority of people in this age category either work part time, or do not work at all. Again, all of this relates to formal employment, so we omit household work, which is important in the economy as well, but is hard to quantify.

With caveats, then:

- Between 2006 and 2009 working age group population in Ireland grew by 189,100 and in the period of 2010-2012 it shrunk by 27,000. Quite a reversal in the 'demographic dividend' if you ask me.

- The same group share of total population grew by 0.1 percentage point in 2006-2009 period and contracted by 1.0 percent in 2010-2012 period.

- Meanwhile, the opposite side of the 'dividend' performed in exactly the opposite direction: non-working age population grew in 2006-2009 period by 114,500 and then again expanded by 57,700 in the period of 2010-2012.

- The share of total population that is captured by the non-working age population shrunk by 0.1% in 2006-2009 period and grew by 1.0% in 2010-2012.

- Let's sum this up: in 2006-2012 period, working age population expanded by 150,800, while non-working age population grew 201,600. If this is a dividend, so far it is coming up negative. Proportion of working age population as a share of total population shrunk 1.5% and proportion of non-working age population expanded by 1.5%.

Charts to illustrate:

The above, of course, leaves out the account of unemployment. But even abstracting away from this, Ireland is now at risk of suffering from rising twin dependency: fewer working-age people funding more non-working-age people. All because of emigration. Dividend...