On November 1, Agustín Carstens, General Manager, Bank for International Settlements delivered a pretty punchy speech on the topic of payments systems evolution in modern age of digital technologies. Punchy, in the sense that much of it is focused on, indirectly, enlisting the evidence as to the lack of the markets for the blockchain and cryptocurrencies deployment in the payments systems at the wholesale and retail levels.

Take the following: "One of the most significant developments in the evolution of money has been its electronification and, more recently, digitalisation. ...Realtime gross settlement (RTGS) systems for interbank payments, ...emerged in the 1980s. ...RTGS systems allow banks and other financial institutions to send money to each other with immediate and final settlement. They are typically operated by central banks and process critical (read: high-value) payments to allow for the smooth functioning of the economy. Today, the top interbank payment systems in the G20 countries settle more than $17.5 trillion a day, which is over 50 times a working day’s global GDP. ...Given the technology cycle, many central banks are currently looking at next-generation RTGS systems to offer more robust operations and enhanced services."

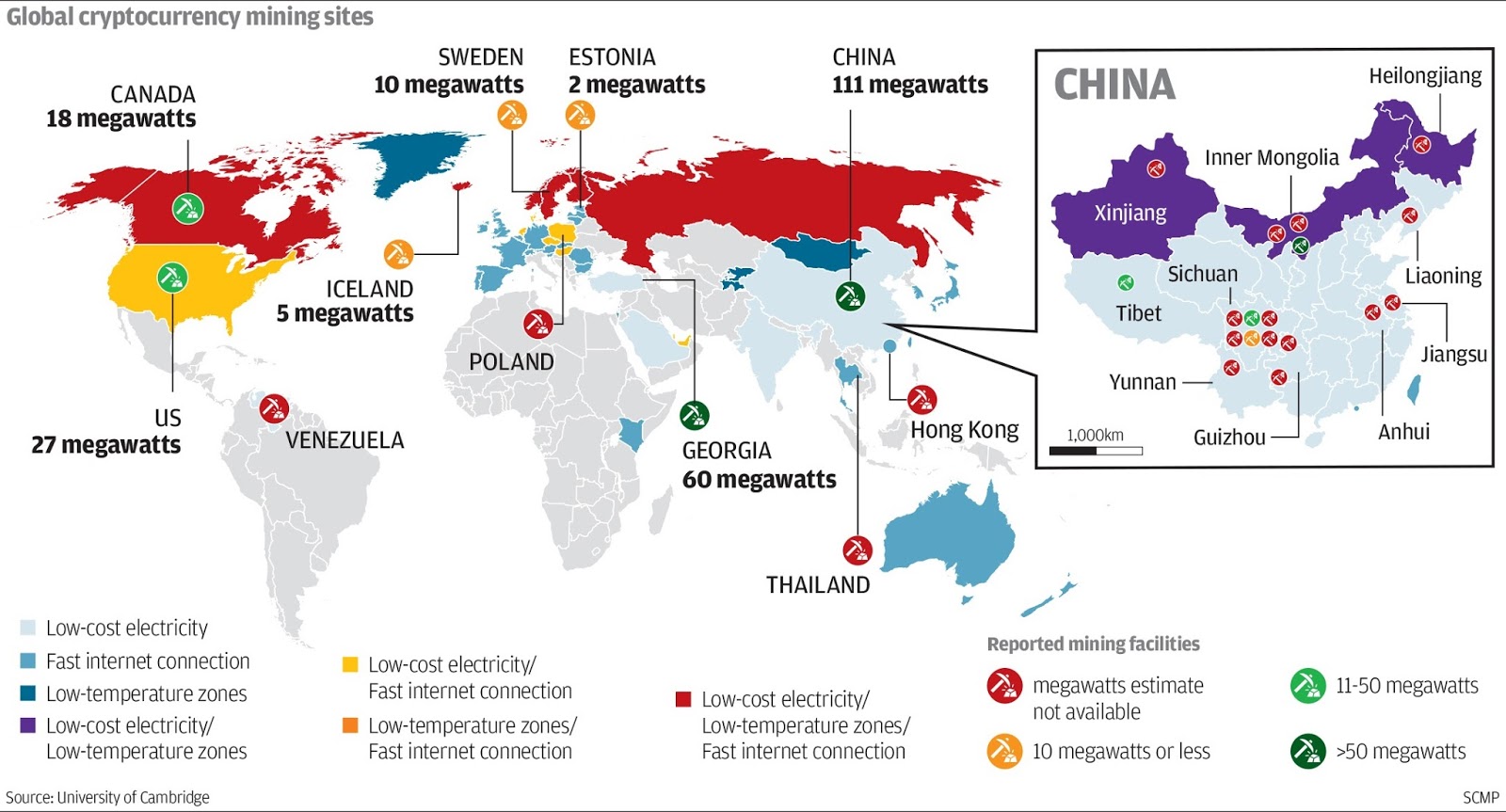

What does this imply for the world of cryptos? In simple terms, there is no market for cryptos as platforms for interbank payments settlements - the market is already served and the speed of services, cost and security are underpinned by the Central Banks.

Next up: retail payments systems.

Starting with back office: "For retail payment systems, ...in Mexico consumer payments operate at the same speed as interbank payments... The beneficiary of a payment is credited money in near real time. That is, if I were to send you money from my Mexican bank account, you would see the funds in your Mexican bank account in 15 seconds or less. ...Based on a BIS analysis, fast payment systems are likely to become the dominant retail payment system by 2023."

Again, what's the market for blockchain systems to be deployed here? I am not convinced there is one, especially as payments latency and costs are, to-date, more prohibitive under blockchain systems than using traditional payments platforms.

Front office: Carstens notes the progress achieved in delivering what he describes as "payments ... made using bank account aliases" in Argentina that are instant in time, and the ongoing trend toward development of the front-end payments interfaces, based on "cashless systems – no cashiers, no lines, no cash, no physical payment devices. Amazon and others envision a future where you walk into a store, take what you want, and are automatically billed for the items using facial recognition and artificial intelligence. Though this approach may seem a bit scary, it is less so than having microchips implanted inside us, which some firms are also piloting! To be frank, though, neither of these options – facial recognition or microchip implants – are particularly appealing to me."

Carstens presents the evidence that shows current Advanced Economies already carrying more than 90 percent of wholesale payments via cheap, lightning fast and highly secure centralized RTGS systems, with 75 percent of payments via the same occurring in the Emerging Markets:

Given this rate of adoption, coupled with the evolving technology curve (that enables similar systems to be deployed in smaller settlements), one has to question the extent to which cryptocurrency solutions can be deployed in the payments systems.

Beyond the not-too-optimistic view of the market niche size, cryptos and blockchain are also facing some serious pressure points from already ongoing innovation in centralized clearance systems. "Although much attention has been focused on cryptocurrencies as the “it” innovation in payments, there’s much unheralded innovation going on" in the Central Banks and elsewhere (read: legacy providers of payments). "Central banks have been pushing the boundaries of what technology can achieve for operational robustness, including switching seamlessly between data centres at short notice and synchronising geographically dispersed data centres."

Carstens notes the potential for the distributed Ledger Tech (aka, blockchain based on private, enterprise-level blockchain) in this space, where innovation is also a domain of the centralized players, as opposed to decentralised crypto markets. "One interesting development in the central banking community is ongoing experimentation with distributed ledger technology (DLT) as a means to enhance operational robustness. People often use DLT and Bitcoin interchangeably, but they are not the same! ...DLT is simply a set of processes and technologies that enable multiple computers to maintain collectively a common database. DLT does not mean mining of coins, public ledgers and open networks. And no central bank that I’m aware of is contemplating these properties in its DLT experimentation."

There are some problems, however, for DLT enthusiasts:

1) "...a Bank of Canada study noting that a DLT-based payment system meeting central bank requirements would be similar to what we have today (ie private ledgers, closed networks and a central operator). The difference is that a network of computers would be used to settle a transaction instead of one computer." In other words, there is a case, yet to be proven, that DLT offers anything new to the payments systems to begin with.

2) "The second is an ECB and Bank of Japan study concluding that processing times would be three times longer using DLT versus current systems." In other words, DLT/blockchain cannot deliver, so far, on its main premise: higher processing efficiency than legacy systems.

Carstens sums it up: "My take is that current versions of DLT are not any better than what we already have today."

In other words: DLT/blockchain solutions appear to be:

- Not necessary: the technology is attempting to solve the problems that do not exist in the payments systems;

- Inefficient with respect to its core tenants/promises: the technology is inferior to existent solutions and the pipeline of ongoing improvements to the legacy systems.

Which begs two questions that the DLT/blockchain community needs to answer: What niche can blockchain occupy in payments systems going forward? and Is there a sustainable market within that niche that cannot be captured by alternative technologies?

But there is more. Carstens explains: "Cryptocurrencies, such as Bitcoin, Ether and Tether, do not serve the core functions of money. No cryptocurrency is a true unit of account or a payment instrument, and we have seen this year that they are a poor store of value. This then raises the question: what are they?" The answer should be a wake up call for anyone still long cryptos: "From my perspective, cryptocurrencies are, at best, an asset of some sort. Perhaps an asset comparable to a piece of art for those who appreciate cryptography. Buyers of cryptocurrencies are buying into nothing more than a software algorithm. Some firms are trying to back cryptocurrencies with an underlying asset, such as cash or securities. That sounds nice, but it’s the equivalent of making art from banknotes or stock certificates. The buyer is still buying an idea or a concept or, if you will, an asset that is the equivalent of art hanging on your wall. If people want the underlying asset, they might be better served just buying that."

Carstens previously (February 2018) claimed that the #cryptos are “combination of a bubble, a Ponzi scheme and an environmental disaster.”

Nice perspective. If you are an observer. For a holder of cryptos, this is a serious risk. Playing cards in a casino is fun, but it is not investing. Playing investing in the cryptos world is probably the same.

Note: for an even more 'in your face' assessment of the #Bitcoin and #Cryptos, there is ECB's Executive Board member, Benoit Coeure, who called #BTC the “evil spawn of the [2008] financial crisis, per Bloomberg report of November 15 (

https://www.bloomberg.com/news/articles/2018-11-15/cryptocurrencies-are-evil-spawn-of-the-crisis-for-ecb-s-coeure).

The reality of #cryptos investments is that they are, empirically, a massively overvalued bet on the largely undeveloped and unproven (in real world applications) technologies that have only tangential relation to the coins currently traded in the markets. It is, in a way, a derivative bet on a future contract.